Capitalism gets into deep trouble when the price of financial assets becomes completely disconnected from economic reality and common sense. What ensues is rampant speculation in which financial gamblers careen from one hot money play to the next, leaving the financial system distorted and unstable—a proverbial train wreck waiting to happen.

That’s where we are now. And nowhere is this more evident than in the absurd run-up in the price of European sovereign debt since the Euro-crisis peaked in mid-2012. In that regard, perhaps Portugal is the poster-boy. It’s fiscal, financial and economic indicators are still deep in the soup, yet its government bond prices have soared in a triumphal arc skyward.

Unfortunately, the recent crash landing of its largest conglomerate and financial group (Espirito Santo Group) is a stark remainder that its cartel-ridden, import-addicted, debt-besotted economy is not even close to being fixed. Notwithstanding the false claims of Brussels and Lisbon that it has successfully “graduated” from its EC bailout, the truth is that the risk of default embedded in its sovereign debt has not been reduced by an iota.

At the time of the 2011-2012 crisis, its central government was already sliding rapidly into a debt trap with a ratio of just under 100%. Self-evidently, the nation’s so-called EC bailout has only made its public debt burden dramatically worse. Today Portugal’s debt to GDP ratio is 129% and there is no sign of a turnaround.

But that has not deterred the rambunctious speculators in peripheral sovereign debt. Since mid-2012 and Draghi’s “whatever it takes” ukase, the price of Portugal’s public debt has soared. This means that leveraged speculators—-and they are all leveraged on repo or similar forms of hypothecated borrowings—-have made a killing, harvesting triple-digit gains on the thin slice of non-borrowed capital they actually have at risk in these carry trades.

As shown below, in response to this central bank induced bond buying campaign by fast money speculators, the 10-year Portuguese government bond yield has experienced a stunning plunge from 15% to 4% during the last 24 months. Among other things, this dramatic improvement virtually overnight in its fiscal financing costs has taught Portugal’s government a dangerously false lesson. Namely, that in the face of unsustainable fiscal profligacy all its takes is a little budgetary sleight of hand and fake austerity. In fact, nearly all of its fiscal improvement is owing to the one-time sale of state assets including the airport operator and various public utilities under financial arrangement which amount to little more than off-budget borrowing.

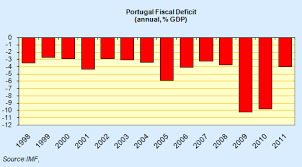

Moreover, regardless of the quality of its fiscal recovery measures, the sharp drop in its bond yield would ordinarily at least imply that Portugal has turned its chronic fiscal deficits on a dime, but that is not remotely the case, either. Portugal has been burying itself in red ink for decades and despite being down from their crisis peak of 10% of GDP in 2010-2011, government deficits, as shown below, are still running at the historic rate of 5% of GDP and will be lucky to break below that level in 2014 or anytime soon thereafter.

Needless to say, when a country’s nominal GDP is stuck on the flat-line, it can’t add 5% of annual output to the public debt each and every year without quickly being doomed by sheer arithmetic. That baleful fiscal math, in fact, is exactly the reason its bonds sold off so sharply in the first place, and why in the absence of massive central bank distortion of bond prices, Portugal would still be under the thumb of crushing yields on its monumental public debt.

So what is at work here is the opposite of is honest price discovery of the type that occurs on a genuine free market. There is virtually no logical basis for the bond market rally in Portuguese or other European sovereign debt. As detailed below, the whole thing is a central bank driven wave of short-term speculation and inflows of hot money which can reverse as quickly as it arrived following Draghi’s ukase.

In the meanwhile, the Wall Street and London sell-side continues to promote hairline and often transient improvements as justification for the rally, which is to say, purchase of bonds and derivatives from their trading desks. In truth, the dismal facts of Portugal’s stunted economy and profligate fiscal practices have barely improved, but that does not prevent sell side ballyhoo from breaking out all over.

During recent quarters, for instance, Portugal’s real GDP has turned slightly upward, but the magnitude of improvement is laughably marginal—-certainly not remotely consistent with the massive gain in its bond prices. Thus, after three quarters of hairline gains, its real GDP in the Q2 2014 was a barely measureable 0.8% larger than the same quarter a year ago. And these rounding error gains, of course, have not yet made up a fraction of the deep shrinkage that occurred in the prior two years.

Indeed, despite all the sell-side drum-beating, Portugal’s real GDP is still 6% smaller than it was on the eve of the financial crisis in 2007. In that context, the galloping bond market rally during the past two years is insensible: a slight uptick from the bottom of a deeply depressed trend is no evidence whatsoever that Portugal’s battered national economy is being sustainably rejuvenated, or that its capacity to service its spiraling debts has been improved in the slightest. In short, the entire bond rally has noting to do with the fundamentals of Portugal’s fiscal and economic circumstances.

The real problem, of course, is that all sectors of the Portuguese economy buried themselves in debt during the years after it joined the EC and was able to access the cheap funding available in the euro bank and bond markets. Indeed, the explosive growth of debt was so extreme that it could be fairly labeled as a sheer financial orgy. As shown below, during the 14 years between 1996 and 2010, for example, household sector debt increased by 6X at a time when the nominal GDP grew by less than 2X.

Even after some modest liquidation during the last 4 years, household debt is still 5X larger than it was in the mid-1990s, yet Portugal’s nominal GDP has actually declined since the 2010 debt peak, meaning that the household leverage ratio is now worse than ever.

The same holds for non-financial business debt, which also soared by 6X after the turn of the century. As is evident below, there has been no progress whatsoever in reducing the enormous burden on the business sector.

Toss on top of this the still rising government debt burden and the implication is obvious. During the halcyon years of Europe’s debt orgy, Portugal went whole hog attempting to borrow its way to prosperity. Now its economy is crushed by the resulting balance sheet fiasco, and shows no signs that its devastating leverage ratios have been reduced by its so-called austerity program.

Indeed, what all this fantastic borrowing did was to allow Portugal to finance a wholly unsupportable national life-style by importing vastly more goods and services than it exported, and financing the difference by means of the above borrowings in the euro debt markets. During the decades leading up to it financial crisis, its current account deficit averaged between 6% and 12% of GDP—surely a dead-end trend if there ever was one.

Once again, however, the sell-side propaganda about the “turn” in Portugal’s current account is just another case of grasping at straws. In order to liquidate its towering debts, Portugal actually needs to run large trade surpluses for years to come in order to generate the means of pay down. But despite a modest uptick in exports, which is inherently constrained by the faltering condition of the EC economies and the general world slowdown, it has barely made a dent in its level of imports. Stated differently, the Portuguese economy continues to live high on the hog as is its debt crisis had never really happened.

The fact is, away from Wall Street’s fatuous focus on superficial, hairline signs of recovery, Portugal’s real economy is still deep in the doldrums. Its industrial production index, for example, is down 5% from 2010 levels and 18 percent from turn of the century levels.

But the most telling indicator is its plunging labor force participation rate. As shown in the graph below, the dramatic plunge since 2000 is even more severe than the ballyhooed decline in the US figure. The reason is that Portugal’s work force has been out-migrating in droves or tumbling into its over-burdened social safety net.

Like, in the US, its recent hairline gains in the unemployment rate—still above 15%—are essentially attributable to a shrinking work force.

This is the crux of the matter. With a declining level of labor input and the unavoidable need for nominal wages—which were vastly inflated during the debt boom—to shrink in absolute terms to more sustainable levels, Portugal’s national income growth rate will flat-line for years to come under the best of circumstances, and will continue to decline in the face of another European and global recession.

Accordingly, there is no relief in sight for its towering leverage ratios in all sectors—government, households and business. In these circumstances, a 4% sovereign debt yield is nothing short of absurd.

The truth of the matter is therefore quite simply. Draghi ignited a short-term buying stampede with his mid-2012 pronouncement. This caused a hot money inflow—especially from dollar based Wall Street speculators and hedge funds. It certainly helped that the latter were drowning in liquidity owing to the Fed’s $85 billion per month of QE purchases and the ready availability of essentially zero cost repo financing.

Indeed, the combination of QE3 and Draghi’s “whatever it takes” amounted to a bugle call to the financial hounds. In short order, the impact was to drive both Euro bond prices and the Euro/USD exchange rate dramatically higher. In fact, between July 2012 and spring 2014, the euro rocketed from 120 to 140 or by nearly 17 percent.

Not only did the resulting combo of a rising euro and soaring peripheral bond prices result in a tsunami of hot money into the euro markets, but it also laid the planking for today’s pathetic excuse that Europe is suffering from an economic affliction that can only be solved with an even more fantastic increase in ECB monetary intervention—-even beyond the financial repression it has in place today including negative deposit rates.

But there is no structural deflation in Europe—just the short-term impact on the rate of price change owing to a spike in the exchange rate that, ironically, resulted from Draghi’s pledge that he would run the printing press at some future date at whatever speed might be necessary to “save” the euro and prop up the sovereign debt of the EC periphery.

In truth, the current “deflationary” scare will soon abate as the euro moves through the 130 mark, and dollar-based speculators are forced to sell their peripheral bonds in order to avoid losses. The trend level of euro area inflation has been, and will remain, in the order of 2.2% per annum since 2000 as shown below. Other than the short-run exchange rate effects on the rate of price change, the idea that Europe is suffering a deflationary crisis is ludicrous.

Accordingly, bond yields everywhere throughout the euro area are distorted beyond recognition. In a recent post, EconMatters laid this out quite comprehesively. The data for all of the major European countries shown below truly describe the mother of all bond bubbles. This is central bank destruction at work on a monumental scale.

From EconMatters.

How to properly value European Bonds This seems to be the biggest question in financial markets for me right now because the math just doesn`t add up any way you slice it. When you look at the pricing for European bonds this conclusion jumps out from an analyst perspective, either European bonds were analyzed and incorrectly priced two years ago, or they are currently being analyzed and mispriced today! Possible Explanations for Large Valuation Gap

One might say it is a little of both, the yields shouldn`t have been that high two years ago, and they shouldn`t be this low right now. However, the gap is just too large from a valuation standpoint to hold much water or relevance here. The next possible answer is that central banks have made interest rates for borrowing money so low that this has incentivized bondholders to accumulate more bonds in search of a yield vehicle to invest this ZIRPMoney.

Also, the US QE Program of $85 Billion per month, much of this money may have found its way into the European banking and financial markets further incentivizing liquidity driven asset purchases of all kinds in Europe. But remember, Europe itself has done very little besides the main weapon of ZIRP compared with the United States, and these are European bonds we are talking about. But if it just comes down to ZIRP offering enough of an incentive to buy what were perceived as risky bonds for investors just two years ago, why weren`t these yields much lower as soon as ZIRP began in Europe?

One answer might be that there was a scale issue regarding liquidity, and ultimately there was a lag effect, until liquidity reached a certain threshold, first of filling the deleveraging credit gap, then there is enough to spill over into alternative investments like chasing yield trades. However this two year period also happened to correspond with the $85 Billion QE policy in the United States, and this seems to have been some of the catalyst for ditching investments like Gold in favor of Yield Investments. There is also this ‘Binary Mentality’ in financial markets in evaluating an investment risk or trading strategy, it is ‘Risk On’ or ‘Risk Off’, ‘Yield On’ or ‘Yield Off’, or European bonds are ‘Safe’ or really ‘Risky’.Fundamentals in Europe Haven`t Changed

However when you look at the fundamentals and compare them to 2012 things haven`t really changed that much in Europe from a ‘getting their financial house in order’ standpoint, and their economies aren’t exactly booming, so these bonds seem as risky now as they ever have been from a solvency standpoint. I realize that the higher yields feed on themselves and make Europe`s outlook worse by some metrics, and that lower yields help alleviate near-term financing concerns from an interest on debt perspective, but the moves in these European bond yields just don`t make sense on a valuation standpoint, who would buy these bonds at current prices and yields?

[Moreover, lower yields may be bad because it allows the governments to put off the much needing structural reforms that are necessary for fixing Europe in the long run.] The possible answer is that banks think that they can front run central banks, beg for QE, and get the central banks to take these bonds off their books. Read More >>> The Bond Market Explained for Mohamed El-Erian How Big can the ECB Balance Sheet Really Get?

But remember Europe hasn`t really done any bond buying program, and it really seems like a big risk to take with your only real out being that Mario Draghi can convince policy makers to buy European bonds in any sizeable scale to make all these bonds good values here. The scale is enormous because the amount of debt that Europe needs to sustain their deficit spending weak economies that are not very competitive from a global standpoint outside of Germany is enormous each year. Furthermore, the ECB is really going to buy “all of these European bonds” from Italy to Belgium?

The math doesn`t add up, just think about the Fed`s 4.5 Trillion dollar balance sheet, how big would the ECB balance sheet need to be to have any real impact in buying all these bonds from the banks that currently hold them? What Will Germany Sign Off On? Would Germany really sign off on this even if it was potentially possible to buy even half the bonds of these European countries?

This just seems ludicrous and I hope this isn`t a real investment rationale for buying all these European bonds, that the ECB is going to take them off their hands regardless of price. The other explanation is that these bond investors think they can get out quick enough, make enough money before ZIRP and the market reverses itself, and basically dump these bonds back onto the market without getting hurt.

However, when you calculate the magnitude of how many bonds were bought all across Europe with deficit spending needed to sustain largess social governments, taking yields down from such heights just two years ago, this is a lot of bonds that will have to be dumped onto the market, what effect is this going to have regarding a tremendous spike in yields during this process? Paper Gains on Bank`s Balance Sheets Likely to Reverse to Actual Losses Again

Remember so far these banks and financial players have gained ‘paper gains’ on their books, they of course book the yield profits, but these are small relative to the price moves in these bonds. However the bonds are still on their books and nothing has changed in Europe and in reality many of these ‘paper gains’ on the books will reverse themselves.

In many cases any financial institution who bought bonds over the last year in Europe at extremely high historical prices relative to recent history and the dire fundamentals of Europe from a debt to GDP standpoint is going to incur massive losses on these bonds that make the banks themselves extremely vulnerable to collapse.

Basically needing to be bailed out all over again, i.e., the collapse of the Spanish Real Estate market, and the after effects of all this bad debt on bank`s balance sheets who had exposure to the overbuilding in Spain.The Problem with Accumulating Assets without regard to Fundamental Value means these Assets are Forever Stuck on the Bank`s Books – Nobody will buy them when they need to sell

But based just on the fact that bond investors have no real clue what any of these bonds should be priced at just in a two year period, I have no confidence that their models over a ten year time period have any validity or insight regarding valuations and sound investment decisions. It seems more likely that somebody in Europe is going to have to take huge haircuts on these bond positions, as unlike Japan Europe relies on external funding for these bonds.

It seems like the likely scenario is that yields start rising slowly at first with the extinction of the massive US QE program in October by the Federal Reserve. And pick up steam as the ECB cannot deliver relative to the expectations already priced into European Bonds, and then the technicals take over fueled by the reality that Europe was never fixed.

This leads to the same scenario for these bonds getting ‘re-priced’ back into the bond market that we had just two short years ago. That most of these bondholders will have to take massive haircuts on these positions, and in two to five years European bonds are back pushing the upper limits of yield once again on an increased insolvency risk profile or EU breakup entirely.

The German Bund is a Long-Term Short over 10-Year Duration

But the one thing that is certain is European bonds are not properly priced today on any scenario. There is a high probability that these bonds are completely worthless in ten years for some of these countries, the math just doesn’t work out in some of these peripheral countries. The German Bund also looks like a short at least back to 1.2% from the current 0.88 % yield for the 10-year duration as the market has really gotten ahead of itself in a slow summer, and as markets often do overshoot based upon one-sided momentum trading.

European Bonds Biggest Bubble in a World of Mispriced Assets

I would also reiterate that most of these European bonds are massive shorts, just take positions, be able to stay in these markets for ten years, and most of these bonds are going to ‘re-price’ back to the fundamentals of Europe and a sustainable risk profile. Any investor buying European bonds at these prices is going to lose money on this investment when they have to sell these same bonds in an escalating yield environment.

More Money Has Been Lost Chasing Yield the last 10 Years than any other Investment Strategy – Yet it Remains one of the most popular – so much for “Prudential Regulation” Janet Yellen as being an Effective Tool for Containing Risk to the Financial System Remember you haven`t made money on a trade until the position is officially closed out, good luck buying European bonds in the biggest bubble of the vast universe of bubbles that currently exist in the financial universe that we find ourselves in due to incompetent Central Banks, matched only by incompetent governments who spend more than they can possibly take in regarding revenue, all cheered on by irresponsible banks who want their investment risk subsidized by others.

I am a finance guy, and the math ultimately has to make sense, and it just doesn`t make any sense in Europe, and unlike the United States, the margin of error for Europe is not nearly as big to fall back on!

Sem comentários:

Enviar um comentário